3 weeks ago

12

3 weeks ago

12

Dear subscribers,

We’re back with a concise briefing for founders, investors, VCs, and regulators across Indonesia, the region, and beyond. Inside: the week’s essential shifts in capital, expansion, partnerships, and policy—distilled for fast decision-making. Enjoy!

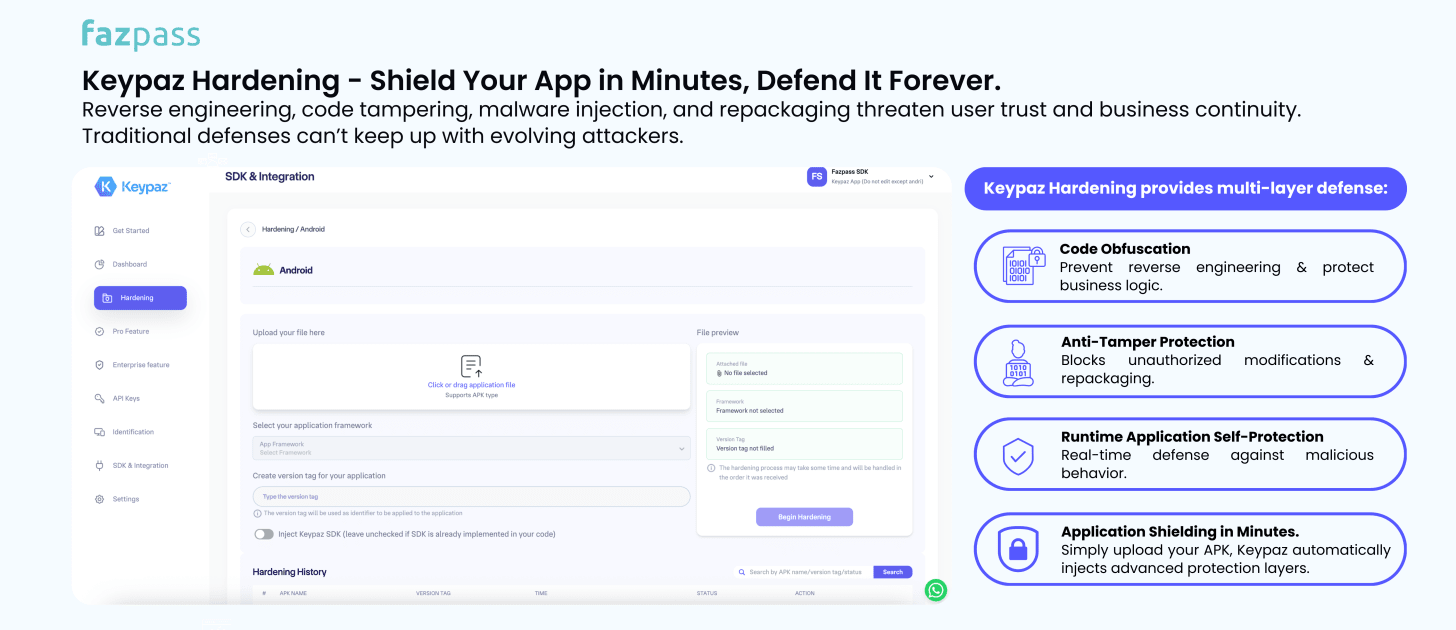

This week’s newsletter is sponsored by Fazpass.

Best regards,

The DailySocial Team

Indonesia launched the Nusantara Lima (N5) satellite on 10 Sep 2025 aboard a SpaceX Falcon 9 from Cape Canaveral. Owned by PT Satelit Nusantara Lima (a PSN subsidiary) and developed with Boeing and Hughes, N5 operates at 113°E with 160 Gbps capacity—the largest in Southeast Asia. The mission is to extend high-speed internet across the archipelago to enable distance learning, telehealth, and MSME digital participation. Early local impacts—such as service improvements at Airu Community Health Center (Papua) and “digital village” pilots in East Java—point to better public services and broader economic inclusion. [Read more]

Bali-based Bliink unveiled a travel-management platform for MSMEs. A companion whitepaper highlights that 97% of Indonesian businesses are MSMEs, most still managing travel manually—leading to up to 30% cost leakage, 60% higher last-minute fares, 1 in 4 employees misclassifying personal expenses, and hundreds of hours lost to manual processes. CEO Larry Chua targets up to 30% savings via corporate fares, policy controls, integrated booking-to-reimbursement (cutting admin time by up to 50%), pay-as-you-go billing, and 24/7 human + AI support. [Read more]

Investors in Kopi Kenangan—including GIC and Peak XV Partners—are exploring partial stake sales with a financial adviser, according to sources. Talks are early and may not result in a deal or defined stake size. A transaction could value the grab-and-go coffee chain at US$1.2–1.4B (subject to change). Founded in 2017, the company operates 800+ outlets across 45 Indonesian cities, with offices in Jakarta, Singapore, and Malaysia. [Read more]

Awanio partnered with Techna-X Berhad and PMBI Technology Sdn. Bhd. (Malaysia) to advance Indonesia’s digital sovereignty through technology transfer, talent development, and a regional innovation hub spanning cloud, virtualization, and AI. The collaboration covers training curricula, Indonesia–Malaysia talent exchanges, and capacity-building for faster, safer cloud adoption in public and private sectors. CEO Irfan Yuta Pratama aims to boost local competencies and regional go-to-market, nurturing competitive “local hyperscaler” capabilities. [Read more]

Carro lines up dual-listing options and Australia expansion

Carro (Temasek/SoftBank-backed) is evaluating a potential dual listing while preparing an Australia launch and 2–3 acquisitions as early as next quarter, said CEO Aaron Tan. The firm is in talks with banks including HSBC and UBS (no advisers appointed yet); possible venues include the U.S., Hong Kong, and Singapore. Tan highlighted a path to US$120–150m EBITDA next year, aided by 20–30% tech-cost reductions from AI adoption. The push follows last year’s Hong Kong entry via the Beyond Cars acquisition and would bring Carro’s full service suite to Australia.

Accion closes US$61.6m early-stage fintech fund

Accion closed Accion Venture Lab Fund II (rebranded to Accion Ventures) at US$61.6m to back ~30 inclusive-fintech startups serving MSMEs and low-income customers across Africa, South & Southeast Asia, Latin America, and the U.S. LPs include FMO, Proparco, ImpactAssets, Ford Foundation, MetLife, and Mastercard. In Indonesia, Accion has previously supported Finfra, Amartha, Semaai, MyRobin, Fairbanc, and Bababos—signaling continued interest in embedded finance and alternative-data solutions, alongside hands-on operational support and networks.

Indonesia’s podcast audience shifts to video

Populix research presented at Radiodays Asia (3 Sept 2025) shows a decisive shift toward video podcasts in Indonesia—“audio-only” listening has more than halved vs 2023. The June 2025 survey of 1,100 Millennials & Gen Z (gender-balanced, mostly employed, upper-middle income, many in Java) finds topic preferences diverge: Millennials lean toward politics/news/motivation, Gen Z toward short-form entertainment/comedy. Two-thirds of video-podcast viewers watch full episodes; others choose by guest—highlighting the power of visuals and star appeal. Monetization is broadening (ad-libs, product placement, logo exposure, affiliate links) as audiences warm to subscriptions/tips; H1 2025 podcast ad spend rose 28% (Magellan AI). Still, over-reliance on ads can pressure quality, making subscriptions a steadier model. Niche shows now reach listeners in 90+ countries.

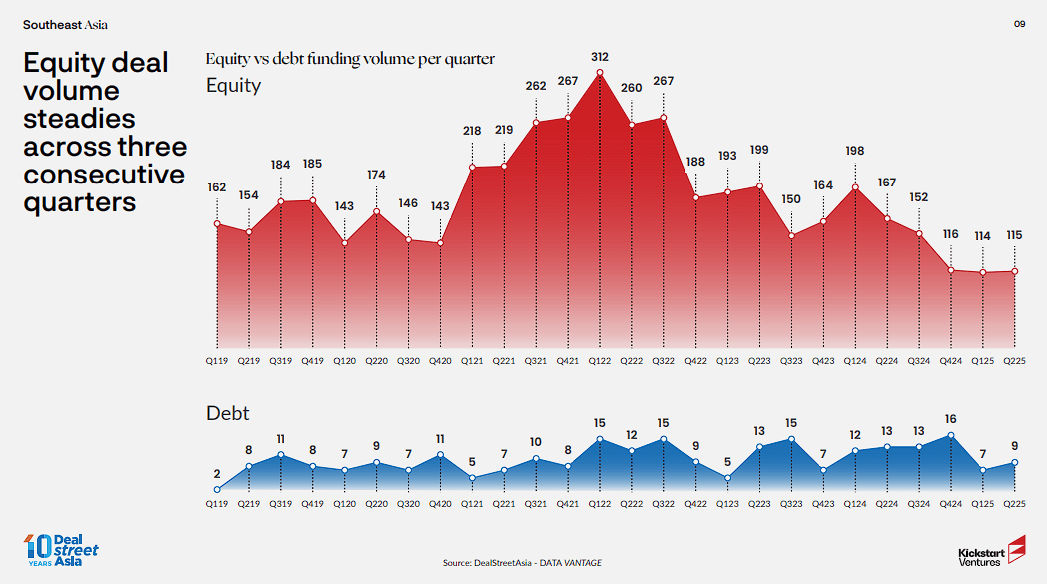

Summarizing the reports of DealStreetAsia and Kickstart Ventures, Southeast Asia’s funding cycle hit a six-year trough in H1’25 at US$1.85B across 229 deals, but momentum improved in Q2 as value more than doubled (US$1.28B vs US$0.57B in Q1)—a sign that capital is concentrating in fewer, stronger companies. Private debt also tightened to ~US$0.49B across 16 transactions, reflecting lender caution and a preference for clearer revenue visibility.

By stage, pressure remained heaviest at the early end. Proceeds to ≤Series B totaled ~US$1.1B, with medians compressing—especially at pre-seed—while investors pushed for disciplined unit economics and governance. At the other end, late stage showed a cautious thaw: 10 deals reached US$756M in H1 with an overall ~US$60M median check, indicating selective conviction in scaled, near-exit stories even as activity remains below historical norms.

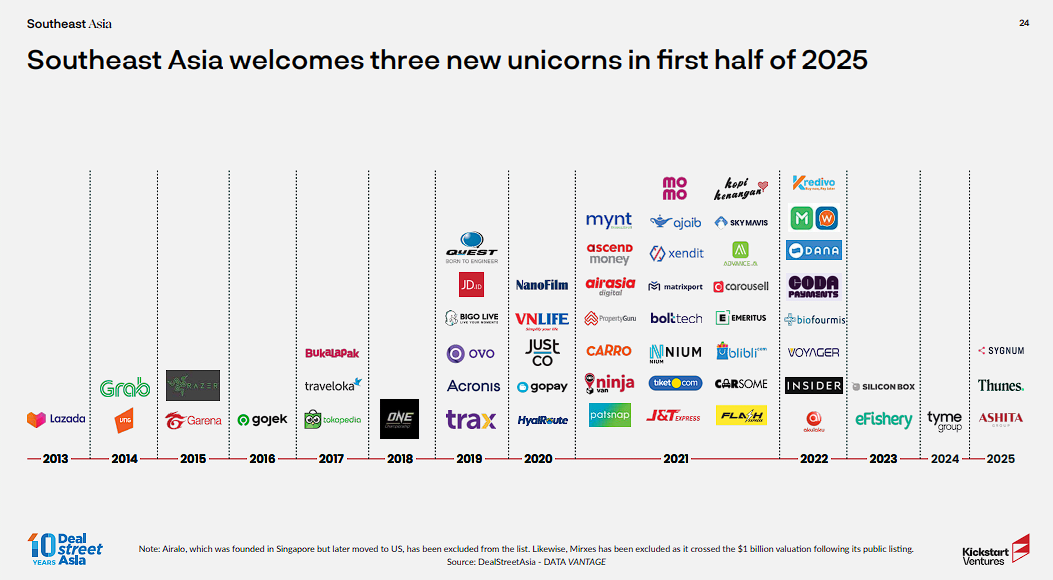

Country mix stayed uneven. Singapore remained the hub (129 deals; ~US$1.206B), Vietnam rebounded (23; US$275M), while Indonesia held 34 deals but slipped on value (~US$78M), trailing the Philippines (US$86M). Despite the slowdown, the region still minted new unicorns (e.g., Thunes, Sygnum), underscoring capital’s flight to quality.

Indonesia’s response is geared to rebuild confidence and improve pipeline quality. On policy, regulators have tightened governance for venture players (e.g., POJK 25/2023) and floated targeted tax incentives to nudge fresh capital back into tech; stakeholder outreach and education are being used to align government and investor expectations while those incentives take shape.

To widen dealflow and international linkages, platforms like the Digital Ecosystem Gathering showcase market depth and catalyze cross-border collaboration. Public–private programs such as BEKUP, Hub.id, DSLaunchpad etc focus on mentoring, upskilling, and investor access so founders become investment-ready faster, while Amvesindo drives governance training and structured dialogues with regulators.

At the demand side, corporate–SOE matchmaking—e.g., Telkom via the investment arms connecting 50+ startups with Telkom BUs and SOEs—helps teams prove revenue and shorten time to institutional funding; sector programs like PLN Startup Day further pull capital toward greentech solutions. These moves, paired with normalizing valuations, aim to channel capital toward startups with proven PMF, capital efficiency, and credible profitability paths.